Every PE deal tells two stories. The first one lives in the information memorandum, clean financials, a compelling growth narrative and a technology section that reads like it was written by someone who has never opened the codebase. The second story lives in the architecture, the vendor contracts and the deployment pipeline. That second story is the one that determines whether the deal creates value or destroys it.

Most PE funds wouldn’t dream of closing a deal without financial due diligence. Legal review is standard. Commercial DD happens on every serious transaction. But technical due diligence, a proper, independent assessment of what the technology actually is, who owns it and whether it can do what the investment thesis needs it to do, still gets skipped more often than anyone in the industry likes to admit.

The cost of skipping it is rarely zero. It just shows up later, when it’s more expensive and harder to fix.

The Information Memorandum Is a Sales Document

This isn’t a criticism. It’s a description.

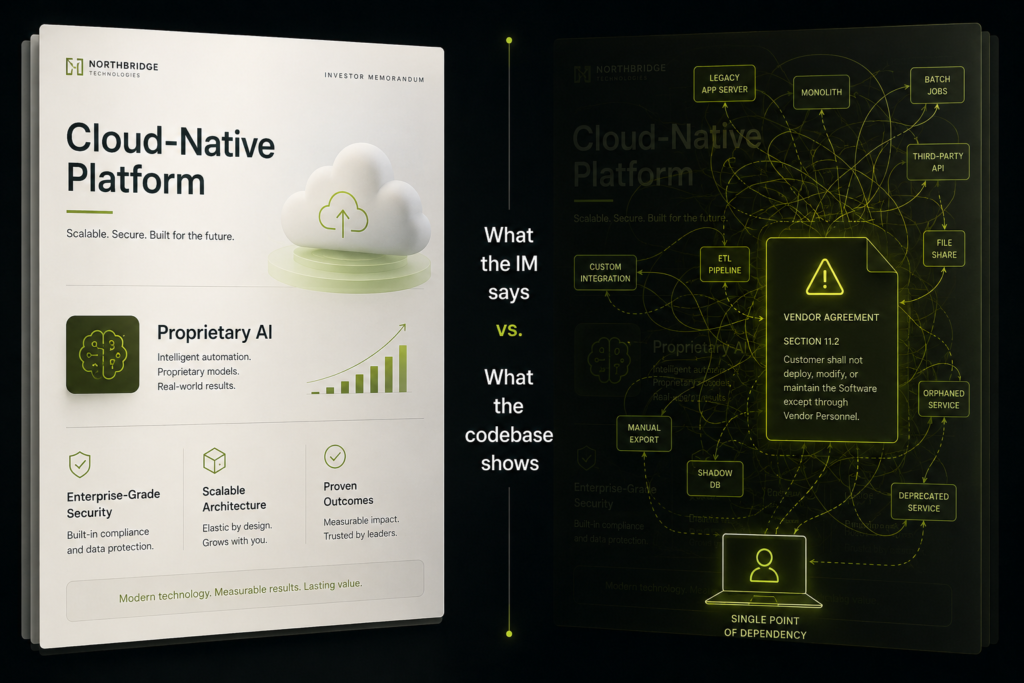

The people who write IMs are not technology assessors. They describe what management believes the technology is, filtered through the lens of what makes the asset attractive to buyers. When an IM says “cloud-native platform with proprietary AI capabilities,” that sentence is doing a tremendous amount of heavy lifting.

Cloud-native implies specific architectural properties, containerized services, horizontal scalability, automated failover, infrastructure-as-code. A platform deployed on AWS EC2 instances is technically “in the cloud.” But it might also be a monolithic application from 2019 running on virtual machines that happen to be operated by Amazon. The distinction between those two things is the difference between a platform that can support the growth thesis and one that needs a rebuild costing crores before it can handle the next tier of enterprise customers.

That rebuild cost is never in the IM. It exists in the codebase, waiting to be discovered by whoever looks.

What Actually Goes Wrong When Nobody Looks

The technology risks that surface post-close follow predictable patterns. After running assessments across dozens of distressed and going-concern acquisitions, the same categories keep appearing.

Vendor dependencies with teeth: A platform’s core differentiator turns out to be a configuration layer built on top of a third-party system. The vendor contract includes a change-of-control clause that triggers renegotiation rights the moment the acquisition closes. The fund valued the capability as a proprietary asset. It was actually a dependency with a price reset built directly into the deal event.

IP that doesn’t belong to the company: The founding CTO left two years ago after a contentious departure. The original employment agreement had an IP assignment clause, but the separation agreement didn’t explicitly confirm that the assignment survived the departure. The core codebase now has disputed or unestablished ownership. In an NCLT or restructuring context, with a departed co-founder who retained lawyers, that gap becomes leverage you didn’t plan for.

Architectural debt disguised as a working product: The platform looks like it works. It does work, as long as the one engineer who understands the deployment process doesn’t leave. The test coverage is 78% on paper, but the payment processing module sits at 11%. The code that handles money, identity and data integrity is effectively untested. Nobody discovers this until the first time a production bug requires modifying that code and the team realizes there’s no safety net.

Each of these findings, individually, might not kill a deal. But they change the economics. And the cumulative effect of two or three of them appearing together can turn what looked like a reasonable acquisition into a capital-intensive remediation project that was never in the model.

The Two-Week Window That Changes Everything

The most common pushback on tech DD is timing. PE deals move fast. Distressed deals move faster. There’s rarely a six-week window for a comprehensive technology assessment and deal teams are understandably reluctant to add another workstream to an already compressed timeline.

But a focused technical assessment doesn’t need six weeks. The three checks that predict deal outcomes most reliably, IP ownership verification, test coverage distribution on critical modules and deployment process dependency mapping, can be completed in under a week. A full assessment covering architecture, security, scalability and team dynamics typically takes two weeks.

Two weeks is not a luxury in a deal timeline. It’s the cheapest insurance available against a write-off that nobody saw coming because nobody looked.

Firms that provide tech due diligence services designed for deal timelines understand this constraint. The assessment has to be fast enough to fit the deal calendar and rigorous enough to surface the findings that change the price, the structure, or the decision to proceed.

What the Findings Actually Do to the Deal

Good tech DD doesn’t kill deals. In fact, the best outcome of a technical assessment is clarity, a clear picture of what the technology actually is, what it costs to remediate the gaps and how to structure the deal to protect against identified risks.

A fund that discovers a vendor dependency with a change-of-control clause before close can add vendor contract novation as a condition of the deal. A fund that finds an IP assignment gap can build a specific indemnity structure into the acquisition agreement. A fund that quantifies the infrastructure rebuild cost can adjust the headline price to reflect the actual capital required.

These are all better outcomes than discovering the same problems after the money has moved.

The deals where tech DD comes back clean aren’t guaranteed to be good deals. But the deals where material findings were missed because nobody checked are almost always more expensive than they appeared. The gap between what the IM described and what the technology actually is, that gap is where the write-offs come from.

Why Financial DD Can’t Catch Technology Risk

There’s a common assumption that financial due diligence will surface technology problems because technology costs show up in the financials. This is true in the sense that a financial model will reflect engineering headcount, infrastructure spend and software licensing costs.

What financial DD cannot do is tell you whether those costs are appropriate for what the technology actually does. It cannot tell you whether the platform can scale to support the growth thesis. It cannot tell you whether the “proprietary” capability is actually proprietary. It cannot tell you whether the departing CTO’s IP assignment documentation has a gap.

Financial DD tells you what the company spends on technology. Technical DD tells you what the company actually has.

Those are different questions. The answer to the first question can look perfectly reasonable while the answer to the second question changes the entire deal.

The Pattern in Distressed Acquisitions

The pattern is consistent across distressed tech acquisitions. The companies coming through resolution processes were built fast, under resource constraints, in a market environment that rewarded speed over architectural durability. The engineering decisions that kept the company alive through its last funding round are the same decisions that created liabilities for whoever acquires it.

Understaffed teams cutting corners for years. Deployment processes that live in one person’s head. Vendor contracts that were signed when the company had no leverage and never renegotiated. IP assignment paperwork that was supposed to get cleaned up during the next funding round, which never came.

None of this is unusual. Companies in distress didn’t get there by building perfect engineering foundations. The question is not whether these problems exist, they almost always do, but whether the acquisition price reflects them.

When the price reflects reality, the deal can still be excellent. The business is real. The customer relationships are real. Under the right ownership with realistic expectations about the rebuild required, the asset has a credible path to creating genuine value.

When the price reflects the IM instead of the reality, the fund is paying for technology that doesn’t exist in the form described. And the difference between those two prices is the write-off that was entirely avoidable.

What PE Teams Should Be Asking

Before submitting a bid on any deal where technology is a material component of the value, three questions deserve specific answers.

First, does the company, the corporate entity, not the founders, cleanly own every piece of IP that makes the product valuable? Pull the registrations. Check the contractor agreements from the first eighteen months. If there are gaps, they need to be resolved before close, not discovered after.

Second, where is the test coverage actually distributed? Not the headline percentage, the breakdown by module. If the business-critical code that handles money, identity and regulatory compliance is below 40% coverage, the remediation cost of bringing it to a responsible level belongs in the deal model.

Third, how many people can deploy the product to production? If the answer is one and that person is considering leaving, the acquirer is one resignation away from a product that cannot ship updates, fix bugs, or deploy security patches. That’s not a theoretical risk in distressed situations where team morale and retention are already fragile.

These three checks take less than a week. They don’t replace comprehensive DD. But they tell you within days whether comprehensive DD is even worth doing, or whether the asset underneath the IM is fundamentally different from what the deal team has been modelling.

The Bottom Line

Technical due diligence is not an overhead cost in a PE transaction. It is the most direct mechanism available for closing the gap between what an information memorandum describes and what the technology actually is.

The funds that run tech DD consistently don’t do it because they’re cautious by nature. They do it because they’ve seen what happens when they don’t and because the cost of a two-week assessment is a fraction of the exposure it identifies.

The deals where nobody looked are the deals where the write-offs come from. Every time.